Posts Tagged "business sale"

14 Reasons Not To Share Ownership with Key Employees

By: Patrick Ungashick

Many business owners consider at some point sharing ownership of their business with one or more key employees. Sharing ownership can create powerful advantages—retaining employees for the long-term is usually a top motive. Sharing ownership appears to elevate top employees into a true partnership with you in the ongoing effort to grow the business.

However, sharing ownership is fraught with potential problems. In our experience, it backfires more often than it succeeds. If it backfires, the owner’s ability to successfully exit from the business one day may be jeopardized.

Listed below are fourteen reasons to avoid sharing ownership with top employees, whether you are contemplating selling or gifting to them a piece of your company:

Top employees sometimes leave. No matter how loyal and trusted they are, be realistic. It happens.

1.Top employees rarely switch industries. If they leave you, they will likely join or become the competition. Now you have somebody competing with you who owns a piece of your business.

2.To prevent this, you will need to have employees sign an agreement obligating them to sell their stock (or units, if an LLC) back to you should they leave. (This is commonly called a buy-sell agreement.) This arrangement helps avoid a competitor owning some of your company. But, you won’t like writing a check to a former employee to buy back your stock. That’s not fun.

3.Speaking of the buy-sell agreement, sharing ownership with top employees increases governance and legal costs, such as creating and/or updating this buy-sell agreement.

4.Sharing ownership complicates decision-making on critical issues, such as selling the entire company one day. You cannot allow minority owners to hold up a possible sale in the future. This buy-sell agreement therefore also needs to give the majority owner clear authority to sell the entire company, further complicating your exit planning.

5.Sharing ownership bestows rights. Even minority owners have certain rights, commonly including a right to review the company’s financial information and records. You may not be crazy about employees seeing that level of financial detail.

6.Sharing ownership with one or more employees creates a precedent. You intend your company to grow, and that growth in the future may lead to additional valuable employees coming into the picture, either hired from outside the company or promoted from within. Those future top employees may want ownership too, given that their peers already have it.

7.Once a top employee has ownership, it’s easy for the line to blur between ownership and employment. It can become harder to manage an employee who also is an owner. Firing that person, if ever necessary, becomes harder and more expensive.

8.With ownership, come perks. You likely enjoy some personal expenses paid by the company, such as your vehicle, cell phone, meals, etc. Employees who receive ownership often expect to participate in such perks. Either, you will have to include them, which increases costs, or you will have to temper their expectations, which increases your work and their disappointment.

9.With ownership comes responsibilities, such as personally guaranteeing company debt. Top employees who have ownership should not be exempted from sharing in the responsibilities and risks of ownership. It takes additional time and work to explain all of this to new owners, and to include them in a creditor’s underwriting procedures.

10.Occasionally, employees might do things that put themselves and their ownership in the company at risk, such as getting divorced, get sued, or find themselves in financial difficulties. Sharing ownership increases the possibility that your company gets dragged into one of these situations.

11.Sharing ownership complicates your tax and wealth planning. Various strategies that owners use to reduce taxes and build wealth get more complicated with more owners. For example, certain laws regarding retirement plans require owner-employees to be treated differently for anti-discrimination testing. Also, if you have an S-corporation and you wish to make a profit distribution, it must be in proportion to ownership.

12.Sharing ownership dilutes your equity position. That can be more expensive than using cash to incentivize, reward, and retain top employees.

13.Sharing ownership can put your exit goals at risk, particularly if you intend to sell the company. Employees with an ownership interest will receive their portion of the proceeds upon sale. Consequently, you may create a situation where these employees are now flight risks immediately after the sale, if they receive enough cash to contemplate leaving the company.

Because of these disadvantages, we try to accomplish business owners’ objectives without sharing actual ownership. Owners and key employees are often surprised to learn that alternative strategies exist which incent and retain top employees, without the risks of sharing actual ownership. One of our favorite tools to reward, retain, and incent employees involves using golden handcuffs plans in lieu of shared ownership.

There are a few situations where sharing ownership with top employees may make sense. The most common would be sharing some actual ownership now as one step within a comprehensive plan to eventually sell or transfer the entire business to the employees. Otherwise, in most cases, it is advisable to pursue a different course of action.

If you have a quick question coming out of this article or, if you want to discuss your situation in more detail, we can set up a confidential and complimentary phone consultation at your convenience contact Tim 772-221-4499

![]()

Seven Situations to Consider Bringing in an Outside Investor

By: Patrick Ungashick

You believe your business would grow faster, if you had more cash.

Or, perhaps you’d buy out that partner who’s not in sync with the company’s direction, if you had more cash.

Or, perhaps you’d take some cash home to diversify your wealth and sleep better at night—if only you had more cash.

Whatever your specific need, perhaps you’d do it—if you had more cash. That’s just the thing though. How do you get more cash to accomplish your business needs, without giving up too much in return, or taking on more risk than you should? Most business owners, at some point, will struggle with this question.

If a need for additional capital is identified, often owners automatically turn to debt to meet the need. Debt avoids dilution. In many cases securing outside debt is easier—one phone call to your commercial banker, and shortly thereafter you have a term sheet in your hand. Finally, owners know that with debt they are not sharing leadership and decision-making control with outsiders.

Yet, there are situations where investigating bringing in outside equity, either as an alternative to debt or as part of combined debt and equity approach, may make sense. We see seven common situations where raising outside equity may be a good fit to meet the needs of the business and its owners:

1.You can bring in outside equity without giving up control. It’s more myth than fact that if you bring in outside investors, you must give up control over your business. While some investors want control, many will consider minority investment situations, and some even prefer it. Most investors will require certain protections, often called “super-majority rights,” that require unanimous consent for the most critical decisions, such as selling the entire company, raising additional debt, or bringing in other investors. But the day-to-day operations and decisions can remain yours entirely in many situations.

2.You have a proven business model with no serious limitations to scalability. If this is accurate, then the more fuel into your company engine, the faster and farther it may go.

3.You have one or more co-owners who are not on the same page with regards to your company’s plans and direction, and buying them out will remove this obstacle and source of friction. With outside capital, you may be able to put cash on the table and buy them out quickly and at an attractive price.

4.You are racing against the competition, and speed to market and/or rapid gain of market share will define success or failure. If this is the case, then you may need to secure sufficient cash to win the race.

5.Your equity partners bring more than just cash to the table. If your investors can bring you market experience, leadership skills, transaction knowledge, industry contacts, or growth opportunities, then you may be getting a bargain. For example, many investors will require a certain number of seats on the Board of Directors. You cannot underestimate the value of having a formal board to help with financing, recruiting, financial and market analysis, project feasibility analysis, legal issues, and exit timing.

6.You desire to “take some chips off the table,” and outside money will allow you to diversify your personal net worth and gain liquidity outside the company. Many owners spend years and sometimes decades highly illiquid. Eventually, this causes most owners personal stress and anxiety—for a good reason. Bringing in outside investors may create personal liquidity, which not only reduces risk but for some owners infuses them with new excitement about taking the company to the next level, given their improved financial security. Bringing in outside investors often eliminates the need for personal guarantees, further reducing the owners’ risk.

7.You have a strong leadership or management team, some of whom want an equity stake in the company. Usually, these leaders and managers lack personal capital to buy into the business. Outside investors can help the management team to buy in, again without requiring taking control. Often we see this done with the current owner maintaining some ownership in the business, allowing him or her to gain liquidity while remaining involved in the company going forward.

There can be additional benefits to bringing in outside equity. One is the potential of increased credibility at your exit. If, after raising outside equity, you later decide to sell the entire company, many buyers have a perception that the business is more “buttoned-up” because outside equity investors have been involved.

While there are other reasons to consider bringing in outside equity, these seven are perhaps the most common situations where outside equity could be a game-changer for you and your company. If you face any of these situations, take an objective, comprehensive review of your company’s capital needs, and then determine the most effective capital strategy—including outside equity when advantageous.

To learn more, watch this webinar on how to “Cash Out Without Walking Out” or contact us with your questions.

If you have a quick question coming out of this article or, if you want to discuss your situation in more detail, we can set up a confidential and complimentary phone consultation at your convenience contact Tim 772-221-4499.

![]()

Your Last Five Years: How the Final 60 Months will Make or Break Your Exit Success

Have you been telling yourself you want to exit from your business sometime within the next “five or so years” for a long time now?

What you do these final five years (60 months) will determine your exit success or failure.

This webinar explains how, and covers:

- Immediate steps to take when you reach five years before exit

- Biggest mistakes owners make, and how to avoid them

- Checklist of things to not overlook

![]()

If you want to discuss your situation in more detail, we can set up a confidential and complimentary phone consultation at your convenience contact Tim 772-221-4499.

![]()

Three Reasons to Take the Surplus Cash Out of Your Company

By: Patrick Ungashick

Too many business owners leave more cash in their company than is necessary. Surplus cash inside the company can cause present and future problems. Here’s how.

First, How Much Cash Does Your Company Need?

Owners and their company’s financial leaders need to answer the question of how much cash the company needs. There are no absolute rules, and every company and industry have specific considerations. Also, how much cash the company needs will change with time as the business grows, market conditions evolve, access to credit changes, etc. While in some cases, the cash question may be difficult to answer; ‘difficult’ does not mean impossible. Leadership teams (with help from outside financial advisors, if needed) must review the company’s recent operations and expected future activities, and then discern how much cash the company needs to meet its operational requirements and growth objectives, with room for a conservative reserve. Many companies have not carefully conducted this analysis or may be working from out-of-date assumptions and paradigms. Once the leadership team has identified the target cash needed, owners should distribute any cash surplus unless there are extenuating reasons not to do so.

There are several reasons why companies might sit on too much cash. A commonly heard justification is holding extra cash helps the owner feel “safe.” Cash is king in times of trouble, so having money readily available in the company’s bank account helps many owners sleep at night. Additionally, many business owners treat “debt” as an altogether bad word. Consequently, the company must hold onto extra cash if there is no sufficient line of credit or other facilities when short term cash is needed. Finally, within entrepreneurial-led companies hoarding cash can be a habit left-over from the days when the company was young and fragile, and founder-owners kept excessive funds as a survival tactic.

Despite these issues, keeping surplus cash in the company is often counterproductive to both immediate and long-term objectives. There are three significant reasons why.

1.Cash in the Company is Exposed to Creditors

Ironically, the feeling that keeping cash in the company increases safety is misplaced. Cash held inside your company is exposed to business creditors, whereas cash held personally is not (unless specifically pledged such as under a personal guarantee). Creditors can be known, like your bank, vendor, or landlord, or can be unknown, acting as a disgruntled former employee or disappointed customer who is preparing to bring a claim against the company. The safest place for cash is likely outside your company.

2.Taking Cash Home Reduces Personal Stress

Many business owners have the majority of their net worth tied up in their company and its supporting assets. This concentration may have caused you little stress when you were younger and tolerated the risk, and when the company’s value was modest. Over time, however, the company grows in value while simultaneously, you get older and perhaps become less risk tolerant. Having a large portion of net worth tied up in the company eventually develops into a stressful situation, for both you and often your family members who share in this risk. Distributing excessive cash can reduce an owner’s stress level and help family members find greater peace of mind.

We see this frequently. A recent former client had a net worth of about $15 million, of which $12 million was the estimated value of his company and the balance mostly tied up in real estate. Troubled by his concentration and illiquidity, the client was rushing to sell some or all of his company. Before committing to a sale, we helped the client identify that his company was sitting on about $2 million in surplus cash. After some cajoling, the client agreed to take a one-time distribution for this amount. After taxes, the client had nearly $1.5 million sitting in his personal bank account. His eagerness to sell the company cooled, and he adopted a more disciplined and less emotional approach to his exit plans.

3.Excessive Cash in the Company Causes Problems at Sale

Excessive cash in the company can become a problem when selling the company. Buyers don’t want to purchase a company stripped bare of cash or cash equivalents—the business must have sufficient working capital to support its operations and expected growth. The funds required to support current and planned operations generally will remain in the company at sale, and thus go to the buyer. Any cash not needed for working capital will be a surplus and typically goes with you the seller.

You can foresee the issue—how much working capital needs to be left in the company will be a point of discussion (and likely negotiation) between you and your buyer. To the extent that you have left more cash in the company than it truly warranted, you have made it easier for the buyer to argue that a more considerable amount of money must be left in the business. That’s the value you would lose. If you find yourself in this situation, to avoid losing that cash, you can have an accounting firm review and reconstruct the company’s actual working capital needs—an expensive project in most cases. The alternative and better solution are to avoid the problem in the first place by not leaving surplus cash in the company.

Getting ready for exit often involves taking steps that seem contrary to how you have managed your company, and your preparations must start no later than five years before you intend to exit. Holding onto too much cash ironically can make it more difficult to exit successfully.

If you have a quick question coming out of this article or, if you want to discuss your situation in more detail, we can set up a confidential and complimentary phone consultation at your convenience contact Tim 772-221-4499.

![]()

Business Valuations: How to Select a Business Valuation Professional

By: Patrick Ungashick

Business Valuations & Exit Planning: A Business Owner’s Guide

This is part four of a four-part series on business valuations, written for business owners who need to understand how business valuations are used in the process of preparing for your business exit. As this series deals with tax and legal subject matters, readers are advised to consult their tax and legal advisors. This material is for educational use only.

How to Select a Business Valuation Professional

There is no such thing as a completely objective business valuation. Every business valuation involves some degree of judgment, which means subjectivity. A human being who values a company has countless decisions and judgment calls he or she must make during the valuation process: which valuation methods to use, what data to include or exclude, how to factor in non-quantifiable issues such as risks, opportunities, market conditions, and more. Even if you are using a software program to do a valuation, subjectivity is introduced by the judgment calls made by the person(s) who programmed the application, and again by the person entering the data. Therefore, if you need a business valuation a critically important question becomes who do you use to do the work?

There is an additional reason to carefully consider who should perform your business valuation. Getting a business valuation is like buying an insurance policy—that valuation may be called up to help protect you against claims against your interests from unfriendly parties, such as a disgruntled business partner, a divorcing spouse’s lawyers, or perhaps even the IRS. Not all business valuations are created equal. The quality of the valuation, and the party who performed it determines how durable that “insurance policy” will be if called upon.

Unfortunately, it’s never been more challenging to determine who you should use to get a business valuation. There are no formal college or university degrees in business valuations, and no state or federal licenses exist. Consequently, many professional advisors will say “Sure, we do business valuations” if asked. An online search turns up countless websites, programs, and calculators that offer low-cost or even free valuations. While free online valuation calculators may be fun to play with, they cannot provide the level of accuracy and assurance that comes with a valuation done by a qualified expert. So, when investigating who to turn to, consider the following:

Professional Experience

While no formal education or licensing requirements exist for business valuations, several organizations offer professional certifications in this field. Look to work with valuation professionals who have at least one of these credentials (listed in alphabetical order):

- Accredited in Business Valuation (ABV). This designation is only to certified public accountants (CPAs) who have passed an exam and have met several thresholds of minimum valuation experience.

- Accredited Senior Appraiser (ASA). To earn the ASA, an applicant must meet specific educational requirements, pass a comprehensive exam, submit their work product to a peer review process, and possess five years of full-time business valuation experience.

- Certified Business Appraiser (CBA). Applicants must meet certain educational requirements, pass a comprehensive exam, and achieve either 10,000 hours of business valuation experience or complete 90 hours of advanced course work. As with the ASA, applicants must also undergo a thorough peer review process.

- Certified Valuation Analyst (CVA). Like the ABV, this credential is only available to CPAs. Applicants must pass a comprehensive exam and complete required course work.

As of the time writing this article, only about 5,000 professionals in the US hold at least one of these credentials. The good news is once you know what to look for, it is not difficult to find them.

How to Find Your Valuation Professional

Should you need a formal business valuation, consider the following steps:

- Ask your existing trusted advisors to refer you to valuation professionals that they know, and hopefully have worked with in prior situations. As a backup method, research online valuation professionals in your area and/or who have experience in your industry.

- Meet or speak with several candidate professionals, share your situation, and ask them how they would approach your needs.

- After initial discussions, ask for a written proposal including a fee schedule and project timeline. Be sure you understand the information and work required of you during the valuation process.

- Once you have selected the valuation professional whom you prefer to work with, have your lawyer review their service contract or agreement. It should contain clear and favorable language about how this professional will respond if called upon to defend their valuation in court, arbitration, or in front of a regulatory agency.

Be sure to review the previous articles in this series (if you have not already) to learn when you might need a valuation, how the valuation process works, and to understand the more common valuation methods. Valuations play an essential role in many business owner’s exit planning process—it pays to know the basics of how they work.

Your Next Steps

Click to register to receive subsequent articles in this series.

If you have a quick question coming out of this article or, if you want to discuss your situation in more detail, we can set up a confidential and complimentary phone consultation at your convenience contact Tim 772-221-4499.

![]()

Business Valuations: Business Valuation Methods

By: Patrick Ungashick

Business Valuations & Exit Planning: A Business Owner’s Guide

This is part three of a four-part series on business valuations, written for business owners who need to understand how business valuations are used in the process of preparing for your business exit. As this series deals with tax and legal subject matters, readers are advised to consult their tax and legal advisors. This material is for educational use only.

Business Valuation Methods

Determining the value of a privately held company is a combination of science and art. Professional appraisers have a toolbox full of valuation methods available to them to calculate the value a company (or in some cases a partial interest in that company.) Applying these methods and doing the math correctly is science. But selecting which method or methods to use is art, because that is determined by the appraiser based on his or her judgement. For you, it is important to know some of the more common methods so you can intelligently discuss them with your valuation professional, because which valuation methods the appraiser uses can produce a dramatically different result. For example, one method might produce a $50 million valuation for a company, while another method might produce a $25 million valuation for the same company—the differences are often that dramatic. So which valuation method, or methods, your professional applies to your company is a critical issue that many business owners overlook or don’t know enough to ask.

There are many valuation methods available to the appraiser, and many methods have several variations. You do not need to be an expert on this topic, but several methods are essential to recognize. They are:

Business Valuation Method #1 – Market Capitalization

Market capitalization, or “market cap,” is arguably the simplest method of business valuation. It is calculated by multiplying the company’s current share price by its total number of shares outstanding at that point in time. For example, if a company’s current share price is $100 per share, and there are one million shares of the company outstanding, then the market cap is $100 million.

Market cap is simple, but it’s typically only applicable to publicly-traded companies because privately held companies don’t have shares traded in the open market. Despite this, it is still important to know what market cap is because part of the valuation process might involve comparing your privately held company to the market cap of publicly traded companies.

Business Valuation Method #2 – Market Value

The market value method attempts to calculate a company valuation based on comparing your company to similar companies in the same industry that have recently been purchased. Market value is perhaps the most subjective method because the professional appraiser must determine and select which companies are comparable despite that in the real world there are no exact matches. Once comparable companies have been identified, then the appraiser must use his or her judgement and apply weighting factors to companies that are dissimilar in characteristics. For example, if your company is doing $25 million in revenue and the valuation professional is looking at data about an industry competitor which recently sold, but this competitor is a $1 billion company, that’s not an apples-to-apples comparison. In that case, the appraiser likely would discount the multiple used on the $1 billion company sale to some lower number applicable to your $25 million company. All of this requires the valuation professional to apply his or her judgement, which is subjective.

All that said, the market value method focuses on understanding what your business might be worth in the open market.

Business Valuation Method #3 – Multiple of Earnings

This method is one of the most important, particularly when considering selling some or all of the company to an outside buyer. Under this method, the company’s recent earnings are applied to a multiplier, which varies with the industry and the economic environment. For example, if the company did $3 million of EBITDA last year and the current multiple for that industry is six, then the potential valuation is $18 million. Typically, the period of time used is the prior calendar year or the trailing twelve months, although if earnings have been volatile over the last few years a weighted average might be used. It is critically important when working with this method that you have accurately calculated your EBITDA, as there are many factors to consider and considerable room for making judgement calls on how certain expenses are treated.

Business Valuation Method #4 – Multiple of Revenue

Under the multiple of revenue method, a stream of revenues (rather than earnings) generated over a certain period of time is applied to a multiplier, which varies with the industry and economic environment. Like with the multiple of earnings method, the period used is commonly the prior calendar year or trailing twelve months, although if revenue has been volatile over the last few years, a weighted average might be used. This method is less commonly used than the multiple of earnings method. It is typically only used in certain industries, such as professional services firms (accounting, legal, engineering, consulting, etc.) and some tech industries.

Business Valuation Method #5 – Discounted Cash Flow (DCF)

DCF is similar to the multiple of earnings method. Using DCF, the valuation professional computes a valuation by taking a projection of the company’s future cash flows, and then discounting them to a single present value—so that cash earned in later years is discounted more heavily than cash earned in more immediate years. The main difference between DCF and the multiple of earnings method is that DCF takes into account inflation and the time value of money when calculating the present value.

Business Valuation Method #6 – Book Value

Book value is simply the value derived by subtracting the total liabilities of a company from its total assets. Book value, therefore, assumes that the company goodwill is zero. Book value is often synonymous with the company’s liquidation value. Book value is typically used in specific situations, such as, companies that have considerable value tied up in their tangible assets. Even when used, book value as a valuation method is not commonly used by itself but rather is often calculated and then included alongside other valuation methods to produce a weighted overall value. (See below.)

This is by no means an exhaustive list of the business valuation methods available to the valuation professional. Also, if you are trying to learn more about these methods take note that different valuation professionals may use different terms to describe the same method, which can be frustrating. However, being familiar with the six listed here provides a foundation from which you can discuss how your valuation professional will select and apply a particular valuation method to your situation.

Business Valuation – A Weighted Approach

Now that we understand there are different valuation methods available to the appraiser, and each method examines different issues and emphasizes different areas, it becomes clear why different business valuations can produce widely varying results even when appraising the same company. To address this, and to create a more balanced and realistic analysis, valuation professionals will commonly calculate a business valuation using multiple methods and then take a weighted average of those methods to produce a final, bottom-line valuation.

While this step reduces some of the disparity between results produced by different methods, it introduces another round of subjectivity into the process as the appraiser has to determine which methods to use, and then how to weight the results. Generally, certain methods tend to earn a greater weighting depending on the nature of the business, the presence or absence of specific data, and the purpose of the valuation. If you hire a valuation professional to appraise your company, it will be vital to discuss which valuation methods are being used and why, and how and why the professional determined the weighted analysis.

Your Next Steps

Click to register to receive subsequent articles in this series.

If you have a quick question coming out of this article or, if you want to discuss your situation in more detail, we can set up a confidential and complimentary phone consultation at your convenience contact Tim 772-221-4499.

![]()

Ever Hear of ZBB? It Can Make You $$$

If you intend to exit by selling your company, either to an outside buyer (a competitor, private equity group, etc.) or an inside buyer (one or more employees), the price you receive at sale will likely be closely tied to the company’s earnings. The higher the earnings, the higher the likely sale price.

As we know, there are two potential ways to grow earnings — increase revenue and decrease expenses. Both methods can maximize earnings prior to selling your business. In our experience, many companies underestimate the amount of expense reduction that is possible prior to selling the company, without harming morale, the team, or key operations.

Remember, if you sell your company for a multiple of six times earnings (commonly calculated as your adjusted EBITDA), then every $1 of expenses you reduce potentially adds $6 to your selling price. Expense reduction prior to sale is a significant opportunity that many owners miss.

How ZBB Can Help Transform Cost Management

That’s where ZBB comes in to help. ZBB stands for zero-based budgeting, and it’s a little-used and often-misunderstood financial management tool. Zero-based budgeting simply means creating an annual budget for the company by starting at dollar zero, then adding expenses into the plan from there.

For each new expense, company management has to justify the item and amount, thus forcing a rigorous and thorough line-by-line examination of expenses that challenges old assumptions and habits each step of the way. (“Why do we spend money on that? Gee, I am not sure. I guess because we always have…”)

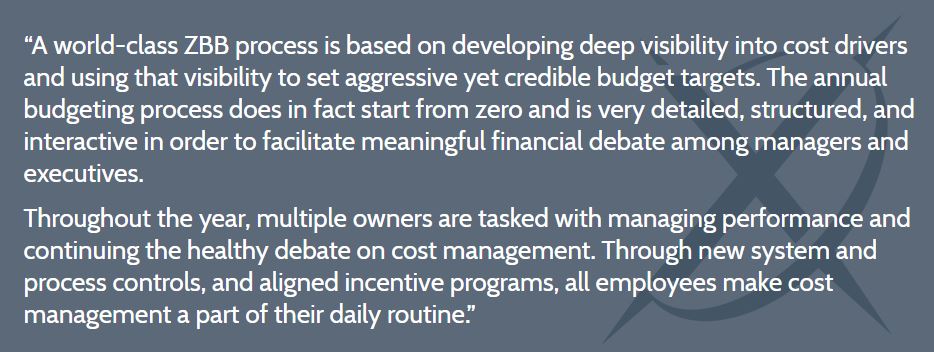

An excellent online article from McKinsey, one of the world’s largest consulting companies, describes how ZBB transforms cost management:

Create a Culture of Accountability and Transparency

Learning and adopting ZBB does not require nor lead to cutting expenses to the bone, as the McKinsey article points out. ZBB compels a more thorough, transparent, and objective look at expenses than many companies would otherwise implement.

When going through a ZBB exercise, it can be helpful to ask aloud “would anybody miss that?” as you and your team consider adding items back into the budget, working up from zero. If you don’t hear a loud outcry within the company that a certain expense would be sorely missed, that’s a clue that the expense in question might be better converted into a savings.

Properly implemented, ZBB is more surgical than draconian, and it can help create a culture of ownership thinking, accountability, and transparency.

Why ZBB Is a Worthwhile Effort

Many business owners, CFOs, and leadership teams are unfamiliar with ZBB and its methods. Some try ZBB but get bogged down in the details. Others fail to realize that ZBB is more than just a financial exercise; implementing ZBB can require rethinking employee communications, internal reporting, and even executive compensation.

The effort can be worth it. Following ZBB practices and principles, it is not usual for companies to realize high single-digit or low double-digit reductions in SG&A expenses. Sustained until company sale, that reduction can generate dramatic returns from increased selling price.

To learn more about ZBB, task the company CFO with studying the issue and reporting his or her findings to the team. There is excellent information online, including the article cited above as well as this article by Forbes. Additionally, contact us at NAVIX to discuss your exit plans and how we can help you and your team maximize your company’s sale price at exit.

To discuss your unique business, and how to plan for and achieve a successful exit, Call 772-210-4499 or email Tim to schedule a confidential, complimentary consultation.

Tim Kinane

Tim is a Consultant to Business, Government and Not-for-Profits Organizations specializing in innovative and challenging ways for organizations to survive, to thrive and to build their teams.

Tim is a Consultant to Business, Government and Not-for-Profits Organizations specializing in innovative and challenging ways for organizations to survive, to thrive and to build their teams.