Posts Tagged "Business Valuations"

Business Valuations: Business Valuation Methods

By: Patrick Ungashick

Business Valuations & Exit Planning: A Business Owner’s Guide

This is part three of a four-part series on business valuations, written for business owners who need to understand how business valuations are used in the process of preparing for your business exit. As this series deals with tax and legal subject matters, readers are advised to consult their tax and legal advisors. This material is for educational use only.

Business Valuation Methods

Determining the value of a privately held company is a combination of science and art. Professional appraisers have a toolbox full of valuation methods available to them to calculate the value a company (or in some cases a partial interest in that company.) Applying these methods and doing the math correctly is science. But selecting which method or methods to use is art, because that is determined by the appraiser based on his or her judgement. For you, it is important to know some of the more common methods so you can intelligently discuss them with your valuation professional, because which valuation methods the appraiser uses can produce a dramatically different result. For example, one method might produce a $50 million valuation for a company, while another method might produce a $25 million valuation for the same company—the differences are often that dramatic. So which valuation method, or methods, your professional applies to your company is a critical issue that many business owners overlook or don’t know enough to ask.

There are many valuation methods available to the appraiser, and many methods have several variations. You do not need to be an expert on this topic, but several methods are essential to recognize. They are:

Business Valuation Method #1 – Market Capitalization

Market capitalization, or “market cap,” is arguably the simplest method of business valuation. It is calculated by multiplying the company’s current share price by its total number of shares outstanding at that point in time. For example, if a company’s current share price is $100 per share, and there are one million shares of the company outstanding, then the market cap is $100 million.

Market cap is simple, but it’s typically only applicable to publicly-traded companies because privately held companies don’t have shares traded in the open market. Despite this, it is still important to know what market cap is because part of the valuation process might involve comparing your privately held company to the market cap of publicly traded companies.

Business Valuation Method #2 – Market Value

The market value method attempts to calculate a company valuation based on comparing your company to similar companies in the same industry that have recently been purchased. Market value is perhaps the most subjective method because the professional appraiser must determine and select which companies are comparable despite that in the real world there are no exact matches. Once comparable companies have been identified, then the appraiser must use his or her judgement and apply weighting factors to companies that are dissimilar in characteristics. For example, if your company is doing $25 million in revenue and the valuation professional is looking at data about an industry competitor which recently sold, but this competitor is a $1 billion company, that’s not an apples-to-apples comparison. In that case, the appraiser likely would discount the multiple used on the $1 billion company sale to some lower number applicable to your $25 million company. All of this requires the valuation professional to apply his or her judgement, which is subjective.

All that said, the market value method focuses on understanding what your business might be worth in the open market.

Business Valuation Method #3 – Multiple of Earnings

This method is one of the most important, particularly when considering selling some or all of the company to an outside buyer. Under this method, the company’s recent earnings are applied to a multiplier, which varies with the industry and the economic environment. For example, if the company did $3 million of EBITDA last year and the current multiple for that industry is six, then the potential valuation is $18 million. Typically, the period of time used is the prior calendar year or the trailing twelve months, although if earnings have been volatile over the last few years a weighted average might be used. It is critically important when working with this method that you have accurately calculated your EBITDA, as there are many factors to consider and considerable room for making judgement calls on how certain expenses are treated.

Business Valuation Method #4 – Multiple of Revenue

Under the multiple of revenue method, a stream of revenues (rather than earnings) generated over a certain period of time is applied to a multiplier, which varies with the industry and economic environment. Like with the multiple of earnings method, the period used is commonly the prior calendar year or trailing twelve months, although if revenue has been volatile over the last few years, a weighted average might be used. This method is less commonly used than the multiple of earnings method. It is typically only used in certain industries, such as professional services firms (accounting, legal, engineering, consulting, etc.) and some tech industries.

Business Valuation Method #5 – Discounted Cash Flow (DCF)

DCF is similar to the multiple of earnings method. Using DCF, the valuation professional computes a valuation by taking a projection of the company’s future cash flows, and then discounting them to a single present value—so that cash earned in later years is discounted more heavily than cash earned in more immediate years. The main difference between DCF and the multiple of earnings method is that DCF takes into account inflation and the time value of money when calculating the present value.

Business Valuation Method #6 – Book Value

Book value is simply the value derived by subtracting the total liabilities of a company from its total assets. Book value, therefore, assumes that the company goodwill is zero. Book value is often synonymous with the company’s liquidation value. Book value is typically used in specific situations, such as, companies that have considerable value tied up in their tangible assets. Even when used, book value as a valuation method is not commonly used by itself but rather is often calculated and then included alongside other valuation methods to produce a weighted overall value. (See below.)

This is by no means an exhaustive list of the business valuation methods available to the valuation professional. Also, if you are trying to learn more about these methods take note that different valuation professionals may use different terms to describe the same method, which can be frustrating. However, being familiar with the six listed here provides a foundation from which you can discuss how your valuation professional will select and apply a particular valuation method to your situation.

Business Valuation – A Weighted Approach

Now that we understand there are different valuation methods available to the appraiser, and each method examines different issues and emphasizes different areas, it becomes clear why different business valuations can produce widely varying results even when appraising the same company. To address this, and to create a more balanced and realistic analysis, valuation professionals will commonly calculate a business valuation using multiple methods and then take a weighted average of those methods to produce a final, bottom-line valuation.

While this step reduces some of the disparity between results produced by different methods, it introduces another round of subjectivity into the process as the appraiser has to determine which methods to use, and then how to weight the results. Generally, certain methods tend to earn a greater weighting depending on the nature of the business, the presence or absence of specific data, and the purpose of the valuation. If you hire a valuation professional to appraise your company, it will be vital to discuss which valuation methods are being used and why, and how and why the professional determined the weighted analysis.

Your Next Steps

Click to register to receive subsequent articles in this series.

If you have a quick question coming out of this article or, if you want to discuss your situation in more detail, we can set up a confidential and complimentary phone consultation at your convenience contact Tim 772-221-4499.

![]()

Business Valuations: How to Value a Business

By: Patrick Ungashick

Business Valuations & Exit Planning: A Business Owner’s Guide

This is part two of a four-part series on business valuations, written for business owners who need to understand how business valuations are used in the process of preparing for your business exit. As this series deals with tax and legal subject matters, readers are advised to consult their tax and legal advisors. This material is for educational use only.

How to Value a Business

To understand business valuations and how they work, it is helpful to understand the general process most valuation professionals (appraisers) use. The process is more involved and collaborative than many business owners expect. To perform a valuation, appraisers usually do not simply gather financial reports, input numbers into a spreadsheet, and then spit out a figure. You the owner, your company management (especially your CFO and/or controller), and your advisors will work closely with the valuation professional at key steps. The general approach consists of:

Getting a Business Valuation Step 1: Define Your Goals

You and the valuation professional start by discussing the project and defining your objectives and purpose for the valuation. For example, why are you commissioning this valuation? Your purpose will guide the process and, may influence the appraiser’s analysis and conclusions where appropriate. For example, are you seeking the valuation for tax planning purposes? Or are you preparing the valuation pursuant to a pending event such as a marital divorce or business partner buy-out? It is imperative that you and the valuation professional understand your goals. The appraiser’s goal then should be to ultimately, deliver to you a comprehensive and defensible business valuation.

(Note: You may have specific assets such as real estate, equipment, or intellectual property held within your company, or owned in another entity and leased back to your company. Depending on your situation the appraiser may need to review these assets as part of the valuation process, and determine a distinct value for them separate from the company’s value.)

Getting a Business Valuation Step 2: Gather Data

Typically, the valuation professional then provides you and the involved members of your leadership and advisory team with a list of required financial reports and information, usually going back three full years. Commonly the appraiser will want to see income statements and balance sheets, but they may ask for additional detailed financial and tax reports. They likely will also ask for non-financial information such as the company organizational chart, business plan, budget, and any industry data or reports you can provide.

The valuation professional will then study and review the information, using questionnaires and templates they have developed for this purpose. They will subsequently meet with you and the company management to ask additional questions to clarify and deepen their understanding of the company, including its strengths, risks, market, and direction. The better the valuation professional understands the financial and operational aspects of your company, the better prepared they are to achieve your valuation objectives and support their valuation conclusions.

It is critically important that your company’s financial reports and records be current, accurate, and formatted consistent with industry norms and expectations. Otherwise, the valuation exercise could end up becoming a garbage-in-garbage-out exercise. The valuation professional may need to make financial adjustments to account for owner benefits, perks, and non-recurring expenses (commonly called add-backs) as well as understand any intangible assets not fully reflected on the balance sheet. The appraiser must also ask about operational and industry risk factors that can substantiate higher or lower valuations. The valuation professional will also ask for projections of the company’s anticipated future financial performance, commonly called pro-forma financial statements. If you and your management team do not currently prepare projections, the appraiser may assist you in doing so if relevant and advantageous.

As you can see, it’s a collaborative process with a lot of back and forth discussion and exchange of information. This presents the opportunity for you and your management team to give the valuation professional your perspective on the company’s strengths, opportunities, risks, and threats.

Getting a Business Valuation Step 3: Further Research and Analysis

From there, your valuation professional now has plenty of data to analyze from these documents and discussions with you and your leadership team. They may need to recast your historical financial statements, which are often prepared with an eye toward tax minimization and may need to be normalized for business valuation purposes. Additionally, the appraiser may need to research external factors such as economic conditions, industry trends, and comparable transactions within your industry. At each step of the way, if the valuation professional has additional questions, he or she likely will be asking you for further information. In some cases, the valuation professional may need data from your other advisors, such as your accountants.

Getting a Business Valuation Step 4: Preliminary Valuation Findings

While different valuation professionals follow different processes, at this point many will now circle back with you and your team to present preliminary findings. Before issuing a final report, the valuation professional may share their initial thoughts and reasoning, in order to gather your reaction and get additional input from you. What will be significant at this point is not just the preliminary valuation, but just as importantly you need to know how the appraiser got to this preliminary valuation amount. This is the time for you and your team to offer additional input to help the appraiser substantiate a higher or lower valuation, if appropriate.

Getting a Business Valuation Step 5: Final Report

Last, the valuation professional now issues a final report. The reports consist of far more than just the bottom-line number, although understandably that’s what you will initially focus on. Valuation reports should cover an analysis of the company’s risk factors, a detailed description of the company and its market position, and a review and assessment of the prevailing economic conditions and industry trends. Recast financial statements and projections should be included in the report. Then, the valuation professional should clearly state what assessment methods they used to determine their conclusion, and why.

Most appraisers will sit down with you, and relevant members of your management and advisory team, to go through the final report. They should explain all the key points and answer your questions.

Getting a Business Valuation: An Important Tip

There is one important tip to consider if you believe you might need a formal business valuation. Contact your attorney and ask him or her about commissioning the valuation study on your behalf. In other words, you pay your attorney the fee for the valuation and, then your attorney hires the valuation professional for you. The potential advantage this creates is, if done properly, the valuation results will come to your attorney and then may be covered by attorney-client confidentiality. This may be important for protecting your interests. For example, suppose your purpose for getting valuation was tax planning related and you were expecting (or hoping for) a low valuation, but the number came in higher than desired. With the valuation covered by privilege, you and your attorney can safely and confidentially discuss the findings and determine your next steps, including potentially trying another appraiser. Or, the reverse scenario could be true. You could have commissioned the valuation hoping for a high number (perhaps if you are expecting to be bought out by a business partner), but what if the valuation comes in lower than desired? Again, having attorney-client confidentiality may preserve options for you. As with all legal and tax issues, discuss this with your advisors.

Your Next Steps

Click to register to receive subsequent articles in this series.

If you have a quick question coming out of this article or, if you want to discuss your situation in more detail, we can set up a confidential and complimentary phone consultation at your convenience contact Tim 772-221-4499.

![]()

Business Valuations: Why and When Do You Need One?

By: Patrick Ungashick

Business Valuations & Exit Planning: A Business Owner’s Guide

This is part one of a four-part series on business valuations, written for business owners who need to understand how business valuations are used in the process of preparing for your business exit. As this series deals with tax and legal subject matters, readers are advised to consult their tax and legal advisors. This material is for educational use only.

Why and When Do You Need a Business Valuation?

Business valuations are like police officers—you can go for an extended period without ever needing one, but when you do it sure pays to have a good one on hand. So, why and when does a business owner need to engage a valuation professional to do a formal appraisal of the company? (Note: In some cases, the valuation may also need to appraise specific assets owned by or used by the company, such as real estate, equipment, and intellectual property.) This article summarizes the circumstances why and when a business valuation may be essential and/or prudent. The article then describes the situations when a business valuation may be unnecessary, or even counterproductive and a waste of money.

Subsequent articles in this series will explain how valuations are done, review the most common valuation methods which you need to understand, and discuss who is qualified to do your business valuation should you need one.

Business Valuations: Nine Situations When You May Need One

There are many situations and reasons where getting a formal appraisal of the company’s value is required or exceedingly prudent to do. Listed below are the nine situations where you are most likely to encounter a potential need for a business valuation, especially in your exit planning:

1.Shareholder/Investor Reporting – If you have outside investors/owners, your legal agreements may require you to have an annual valuation for shareholder reporting and meetings.

2.Lender Requirements – In some situations, a bank or other lender may require you to get a business valuation up front or perhaps even regularly such as once per year. (Note: It is more common that a lender will require audited financial statements rather than an appraisal.)

3.Stock Options Plans – If you have a stock options plan for your employees, you may be required to get a third-party valuation each year to comply with 409A regulations.

4.ESOPs – ESOPs (employee stock ownership plans), a tactic to help sell your company to your employees, are required to do an annual valuation to establish the per share value of the company.

5.C-Corp to S-Corp Conversions – If you are converting a C-corporation to an S-corporation, a valuation is required at the time of conversion to determine the potential built-in-capital-gains tax.

6.Gifting Ownership – Another tax-related situation involves gifting company ownership to your children, a charity, or perhaps a trust as part of your estate planning. When making gifts of company ownership, a formal business valuation may not be legally required but usually is highly prudent.

7.Bonusing Ownership to Employees – If you intend to bonus ownership of the company to certain employees, a valuation may be advisable to introduce a third-party estimate of the value of the bonused interest and to help determine the tax impact of the transaction.

8.Co-Owner Transactions or Disputes – In situations involving ownership changes between business partners (co-owners), it may be helpful to secure a third-party valuation to determine the price for any interest to be bought or sold between the co-owners. If the situation has become contentious between the co-owners, perhaps to the point where arbitration or litigation may be considered or involved, a valuation is likely even more beneficial.

9.Marital Divorce – If an owner is contemplating or facing a marital divorce, a business valuation is prudent to aid in the negotiations between the couple, or to be incorporated into any legal proceedings.

There are other reasons that a business valuation may be needed, but this list summarizes some of the more common issues that owners potentially encounter over the course of their career, particularly as you plan for your future business exit.

Business Valuations: Three Situations When You Might Not Need One

There are other situations where a business valuation may come up for consideration. Within our organization, we sometimes see a rush to go get a valuation in some circumstances where the need is less clear. Listed below are three situations where, in our opinion, a valuation may be unnecessary or even counterproductive.

1.You are Getting Ready to Sell the Company – One of the more commonly held views as an owner prepares to sell the company, is that you should pay to have a formal appraisal done prior to sale. Presumably, this is to identify the potential sale price and set realistic expectations. Most of the time, we disagree with this approach as unnecessary and even misleading. First, it is typically unnecessary because if you are working with experienced M&A advisors, they should be able to give you an estimated range they expect the company could sell for in the current environment. This is not the same as a formal appraisal, but usually, it is sufficient to set realistic sale expectations. Second, a formal appraisal before marketing the company can be misleading because what your company is worth to an outside buyer is what that buyer will pay for it. Period. The existence of third-party valuation claiming that your company is worth $X amount will not cause a potential buyer to increase its offer price by $1 more than it is otherwise willing to pay.

2.You are Curious – We frequently speak with business owners who have paid for business valuation at some point in the past simply to help them know what their company was worth at that point in time. It is helpful to have a realistic understanding of your company’s value periodically. However, keep in mind that all valuations ultimately involve somebody’s judgement, and have a subjective element. Paying thousands to tens of thousands of dollars to have a valuation done just to get somebody’s opinion about what the company is worth (even an expert assessment) is often not necessary, because alternative methods are commonly available for no cost. For example, researching sale multiples in your industry (usually tied to EBITDA) can produce an approximate value range for your company based on that data. Clearly, this is not the same depth of analysis nor precision that is provided by a formal appraisal. But a market-based estimate will give you a general understanding of company value on a periodic basis—without the cost of an appraisal.

3.You Want to Track Company Growth – This need is similar to “You are Curious” in that you have no specific event or transaction in mind, but rather you seek the benefit of a realistic understanding of changes in the company value over time. Like with the “curious” example, often paying for a formal appraisal is unnecessary. Rather, carefully research sale multiples for your industry and then apply those multiples to your company performance. In this manner, for little time and no cost, you can approximate company value in most cases, and track its changes over time.

Your Next Steps

Click here to register to receive subsequent articles in this series, where we will examine how valuations are done, the most common valuation methods used, and who is qualified to do business valuations.

If you have a quick question coming out of this article, or, if you want to discuss your situation in more detail, contact Tim 772-221-4499 set up a confidential and complimentary phone consultation at your convenience.

Why It May Seem Like Buyers Are Nuts Regarding Your Business’s Value

Recently we had a client go through a thorough and well-prepared process to sell his company. About 300 potential buyers were contacted — a mix of strategic and financial players. Here’s the preliminary breakdown:

- 300 potential buyers contacted

- 78 were interested/requested further information

- 22 held preliminary phone calls with us

- 9 made an initial offer

If we pause right there, the story might seem strange to many business owners. Only nine out of about 300 qualified buyers made an offer for this profitable, growing, and well-organized company. That’s 3%, which means 97% passed.

To many owners contemplating selling their company, to have so few potential buyers actually step up and make an offer seems surprising and more than slightly disappointing. Yet these numbers are quite typical.

The vast majority of potential buyers at any point in time will not pursue buying your company if contacted because they don’t see a strong fit, are occupied with other acquisitions, are undergoing internal leadership changes, are conserving cash, or any number of other reasons.

Buyers (Usually) Aren’t Crazy, They’re Just Very Different

But this typical client’s experience got even nuttier once the offers came in. Here are the nine offer prices listed from lowest to highest:

$5.9 million

$8.0 million

$12.2 million

$12.3 million

$14.1 million

$14.5 million

$17.5 million

$20.8 million

$32.5 million

How does that happen? How can nine potential buyers, all of whom can do math, produce offers that range from a low of $5.9 million to a high of $32.5 million? Are some of them crazy or incompetent? Are the low offers unjustifiably low — or are the high offers dangerously excessive? Or both?

What is going on here? This company had consistently strong earnings, was growing, and was well led. Why was there so much variation in the buyers’ perception of business value?

Buyers are not crazy — usually. And these results are common. What your company is worth varies greatly from buyer to buyer because each buyer comes with a unique set of needs, challenges, strengths, opportunities, and priorities.

These differences lead buyers to conclude widely different valuations when offering to purchase the company in question. For example, the two buyers with the highest initial offers ($20.8 million and $32.5 million) both had excellent distribution systems and saw a massive opportunity to take our client’s proprietary products into their existing markets, generating highly profitable growth through cross-selling.

The remaining other potential buyers either did not see the same opportunity or were not in a position to capitalize on it. Out of the lowball offers, one potential buyer saw little value in our client’s company beyond its asset base. Another low offer came from a buyer that seemed internally disorganized and thus could not get its act together.

The point here is that buyers are not nuts, they are just very different. Their differences often translate into different conclusions on your company’s value and subjective worth to them.

3 Key Takeaways for Owners Expecting to Sell Their Company

There are several important takeaways for business owners expecting to sell their company at some point in the future. They are listed below, in no particular order, along with additional educational resources from us to help you learn more.

1. Very rarely does it pay to talk to just one buyer at a time because without any comparison, you cannot know if that one buyer is your best option or not. Unfortunately, many owners make this mistake. Buyers know this and try to lure owners into these one-way situations. Watch our webinar to learn more about this issue and to learn when you can safely talk to just one buyer.

2. You must be prepared to run a thorough sales process in order to find your best buyer. This webinar has several real case studies that demonstrate ways to find your “unicorn” buyer.

3. While buyers have different needs and priorities, most buyers agree that certain characteristics make a company more or less valuable. For example, a company that is growing and has a diversified customer base will generally be seen as more valuable than a similarly sized company in the same industry that is shrinking and has a narrower customer base. To learn about 25 factors that can drive company value, download this free tool.

Ultimately, the sooner you start preparing for exit, the more time you’ll have to maximize value in your company and find your best buyer. Contact us to discuss your situation and learn how we have helped other business owners maximize their business value.

To learn more about the steps necessary for a successful exit, contact Tim for a complimentary consultation: 772-221-4499 or email.

Ever Hear of ZBB? It Can Make You $$$

If you intend to exit by selling your company, either to an outside buyer (a competitor, private equity group, etc.) or an inside buyer (one or more employees), the price you receive at sale will likely be closely tied to the company’s earnings. The higher the earnings, the higher the likely sale price.

As we know, there are two potential ways to grow earnings — increase revenue and decrease expenses. Both methods can maximize earnings prior to selling your business. In our experience, many companies underestimate the amount of expense reduction that is possible prior to selling the company, without harming morale, the team, or key operations.

Remember, if you sell your company for a multiple of six times earnings (commonly calculated as your adjusted EBITDA), then every $1 of expenses you reduce potentially adds $6 to your selling price. Expense reduction prior to sale is a significant opportunity that many owners miss.

How ZBB Can Help Transform Cost Management

That’s where ZBB comes in to help. ZBB stands for zero-based budgeting, and it’s a little-used and often-misunderstood financial management tool. Zero-based budgeting simply means creating an annual budget for the company by starting at dollar zero, then adding expenses into the plan from there.

For each new expense, company management has to justify the item and amount, thus forcing a rigorous and thorough line-by-line examination of expenses that challenges old assumptions and habits each step of the way. (“Why do we spend money on that? Gee, I am not sure. I guess because we always have…”)

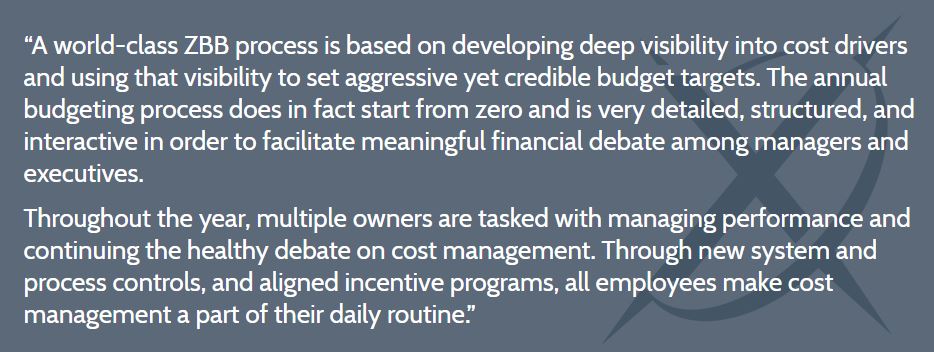

An excellent online article from McKinsey, one of the world’s largest consulting companies, describes how ZBB transforms cost management:

Create a Culture of Accountability and Transparency

Learning and adopting ZBB does not require nor lead to cutting expenses to the bone, as the McKinsey article points out. ZBB compels a more thorough, transparent, and objective look at expenses than many companies would otherwise implement.

When going through a ZBB exercise, it can be helpful to ask aloud “would anybody miss that?” as you and your team consider adding items back into the budget, working up from zero. If you don’t hear a loud outcry within the company that a certain expense would be sorely missed, that’s a clue that the expense in question might be better converted into a savings.

Properly implemented, ZBB is more surgical than draconian, and it can help create a culture of ownership thinking, accountability, and transparency.

Why ZBB Is a Worthwhile Effort

Many business owners, CFOs, and leadership teams are unfamiliar with ZBB and its methods. Some try ZBB but get bogged down in the details. Others fail to realize that ZBB is more than just a financial exercise; implementing ZBB can require rethinking employee communications, internal reporting, and even executive compensation.

The effort can be worth it. Following ZBB practices and principles, it is not usual for companies to realize high single-digit or low double-digit reductions in SG&A expenses. Sustained until company sale, that reduction can generate dramatic returns from increased selling price.

To learn more about ZBB, task the company CFO with studying the issue and reporting his or her findings to the team. There is excellent information online, including the article cited above as well as this article by Forbes. Additionally, contact us at NAVIX to discuss your exit plans and how we can help you and your team maximize your company’s sale price at exit.

To discuss your unique business, and how to plan for and achieve a successful exit, Call 772-210-4499 or email Tim to schedule a confidential, complimentary consultation.

Six Misconceptions About Business Valuations

When do you need to get a business valuation?

Many exit planning books, websites, and advisors recommend getting a business valuation as one of the first steps in exit planning, if not the very first step. At NAVIX, we disagree. While business valuations are a critically important tool in certain situations, business owners should not rush into getting a valuation without careful consideration. The following six misconceptions explain why.

Misconception #1

A business valuation reveals what your company will be worth at sale.

Unfortunately, the only way to know what your company is worth at sale is to enter the market and see what potential buyers are willing to pay for it. While an appraisal by a valuation professional might produce a figure that is close to what some buyers might pay, not all buyers are the same. Buyers have different needs, interests, resources, and potential synergies. This is why it is not unusual to receive a wide range of offer prices when multiple buyers are bidding on the same company. A business valuation cannot anticipate every buyer’s motives and therefore cannot be expected to forecast a company’s final selling price.

Misconception #2

Business owners should get a business valuation at the beginning of their exit planning.

Getting a valuation at the start of one’s exit planning is unnecessary most of the time and might even be potentially harmful. At the start of your exit planning, you might not yet know if you need your valuation to aim high or low. What a business is worth is in part subjective. If you ultimately decide to pursue selling your business to an outside buyer, you hope and aim for a high potential price. But what if you decide to give the business to your children? If that proves to be your exit strategy, you will want an appraisal to aim for the lowest reasonable company value. To further complicate matters, if your exit strategy is to sell to an inside buyer (one or more employees), then depending on the circumstances the desired value could be high or low. Even if you believe that you know your exit strategy at the start, it’s not uncommon for owners to later change their exit strategy once they dig deeper into the exit planning process.

Getting a valuation right at the start of your exit planning is usually premature. You may waste time and money getting a valuation that aims in the wrong direction, and unfortunately once acquired, you cannot make the valuation just go away. Somebody, such as the IRS, may later ask to see that valuation and you might regret what it says.

Misconception #3

Having a business valuation will help you negotiate a higher price.

If, while attempting to sell your company, you find yourself negotiating with a buyer whose offer price is lower than your liking, you could try to get the potential buyer to increase its offer price by producing a third-party valuation that assigns a higher value than the initial offer. However, this tactic is unlikely to create much leverage for you. Most buyers will feel little pressure to raise their purchase price because the valuation comes from a third-party without a vested interest. A superior way to create leverage is to have multiple buyers competing to acquire your company, so that a bidding war ensues. Competition maximizes your leverage.

Misconception #4

Business valuations used for one purpose can be relied upon for another purpose.

Recently, a business owner whose company is partially owned by an ESOP (employee stock ownership plan) found himself in the midst of a divorce. ESOP companies are required by law to have an annual business valuation. This company’s most recent valuation calculated a total value of $10 million. The owner assumed that $10 million would be the value upon which his divorce would be settled. However, things became contentious and the divorcing couple ended up court. The divorce court ordered a new valuation, which came in at more than $30 million to the owner’s shock and dismay.

There are different methods to value a company, any one of which can produce a greatly different figure. For example, a privately-owned company’s value could be calculated based on its future earnings potential, its comparable market transactions, or its assets—or some combination of these three methods. Furthermore, valuations grow stale with time. A valuation done as recently as six months to a year earlier might be irrelevant if business or external conditions have changed. If a valuation was acquired for one purpose, it cannot be assumed that the valuation will be applicable or respected in other situations.

Misconception #5

Use a business valuation to keep score on how your company is performing.

We see this suggestion often. The idea is to get a valuation once a year (or sometimes even more often) to track and evaluate the company’s growth and the performance of its leadership team in particular. In fairness, publicly-traded companies are able to rely on this strategy because the stock market provides constant feedback on the company’s progress and value.

With privately-held companies, however, this tactic has two problems. First, as stated in Misconception #2 above, depending on your ultimate exit strategy you may later regret having on record those valuations stating the company is worth $XX amount. Second, in most situations this simply wastes money when a free alternative exists. All privately-held companies can and should track the key operational, sales, and financial metrics that drive healthy business growth. These metrics can be summarized on a dashboard to provide accurate and timely feedback on business progress and leadership team performance. This not only saves you the cost of a valuation but also provides leadership teams with an actionable tool for tracking performance.

Misconception #6

If a valuation is needed, you should hire the appraiser.

There are valid and important reasons to get a formal business valuation. Three of the more common reasons are:

- It is required for regulatory compliance (such as with ESOPs).

- You are doing important tax planning that requires establishing a business value.

- You are seeking to minimize or resolve contention between interested parties such as spouses or business co-owners.

If facing one of these situations, getting a business valuation is prudent and usually necessary. However, do not hire the valuation professional on your own. Speak with your legal advisors first. It may be beneficial to have your attorney hire the valuation professional and receive the appraisal on your behalf. When having a valuation done, it’s impossible to predict the outcome. The final number may be what you expected, or it might come in significantly higher or lower than desired. If your attorney commissions the appraisal, the valuation’s findings may be protected by attorney-client confidentiality, meaning you will not have to disclose its results to an outside party. Again, it’s important to consult your attorney on these issues.

In summary, business valuations are an important tool in the exit planning process but should not be your first step. Before getting a valuation, owners should clearly define their exit goals and plans. Then, owners can work with their tax, legal, and exit advisors to determine if a valuation is needed and the best course of action to follow.

![]()

To discuss your unique business, and how to plan for and achieve a successful exit, Call 772-210-4499 or email Tim to schedule a confidential, complimentary consultation.

Tim Kinane

Tim is a Consultant to Business, Government and Not-for-Profits Organizations specializing in innovative and challenging ways for organizations to survive, to thrive and to build their teams.

Tim is a Consultant to Business, Government and Not-for-Profits Organizations specializing in innovative and challenging ways for organizations to survive, to thrive and to build their teams.