Posts Tagged "Should You Be a C-Corporation"

Exit Planning Under the New Tax Laws: Should You Be a C-Corporation?

While there are many material differences between C-corporations and other legal forms, for this purpose the most important tax difference is that C-corporations pay taxes on income, whereas the other commonly used legal forms are pass-through entities, which mean taxable income (or losses) “pass-through” to the owners’ personal income tax returns. This difference is relevant because, despite the much-hyped tax cut, owners of C-corporations still face under the new tax laws the risk of double-taxation when they sell the company. If double-taxation sounds bad, that’s because it usually is.

Here’s what double-taxation means, and why it occurs. When corporations are sold, the buyer has a choice to make. Does the buyer want to purchase the corporation’s stock from whomever or whatever owns it, or does the buyer want to purchase the company’s assets from the corporation itself? The two options are thus called stock sales (a.k.a. entity sales) and asset sales. Buyers overwhelmingly prefer asset sales, for two main reasons. First, stock sales increase potential risk to buyers, because if they buy the stock, they may inherit future liabilities attached to that stock, whether known or unknown at the time of sale. The second reason buyers overwhelmingly prefer asset sales is because asset sales typically are more attractive to the buyer financially. In an asset sale, the buyer gets to depreciate on its tax return some assets faster than it commonly would be able with a stock sale. For these two reasons, buyers prefer asset sales.

Are you familiar with the adage that says in any negotiation between two parties where one has all of the money, and the other does not, the one with the money wins? Well, the adage applies here. The buyers have the money. So, more often than not, buyers get their way and require asset sales. (There is even a provision of the tax code called Section 338(h)(10) that lets buyers treat the sale as if it were an asset sale for tax purposes, even though structurally the transaction was a stock sale. This is called a deemed asset sale.)

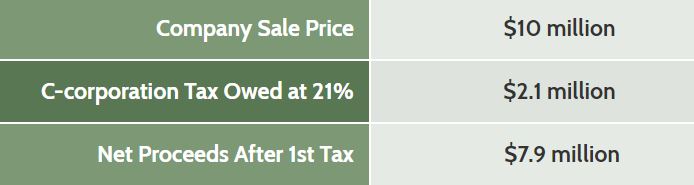

So that means if you intend to sell your company one day, the future sale most likely will be an asset sale. That’s when double-taxation kicks in. First, the buyer purchases from the corporation its assets. At that point, a C-corporation now has to pay any taxes owed from the sale of its assets. Let’s create a simple example. Assume a $10 million asset purchase price, and the company pays exactly 21% in taxes, which is $2.1 million.

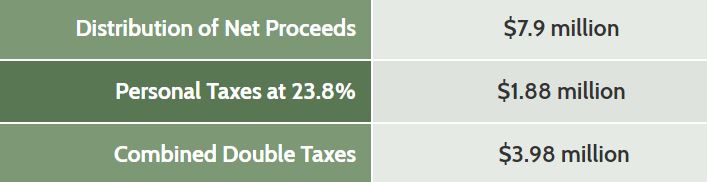

Once the dust has settled, the seller is now left with an empty C-corporation, other than the $7.9 million in after-tax cash from the sale proceeds sitting in the company’s bank account. At that point, the seller wants to take money home thank-you-very-much, and so distributes the money out to the owner(s). That triggers the second tax. Let’s assume that second tax is all long-term capital gains taxes at 20%, plus the 3.8% Net Investment Income Tax that usually applies. So now that’s another $1.88 million in personal taxes ($7.9 million X .238) as shown below. Put the two levels of tax together, and the total taxes paid at sale are about $3.98 million on the original $10 million sale.

The double-taxation creates almost a 40% total tax burden—and this example does not include any state or local taxes, which would only add to the total. So, even though the C-corporation tax rate is reduced, if you intend to sell your company one day to an outside buyer, it remains highly disadvantageous to sell your business while a C-corporation in most situations.

One last important point to remember: If you have a company that is a C-corporation that you expect to sell, and to avoid double-taxation you usually would convert that C-corporation into an S-corporation. However, you must outwait that conversion by five years to eliminate all risk of double-taxation at sale. This arcane tax provision is called the Built In Gains tax—yes, the BIG tax. We can’t make this stuff up.

Operating as a C-corporation may only be advantageous if you are confident that you will not sell the company for any reason within the next five years, or if you never intend to sell your business but instead you give it to family members in the future. All of this reinforces that business owners need to think through their exit and plan ahead on tax questions, many years prior to exit.

This information is for educational purposes only. Please consult your tax, legal, and other advisors to evaluate how this material may apply to you and your businesses. NAVIX does not provide tax or legal advice nor services.

Call 772-210-4499 or email Tim to find out more about exit planning solutions.

Call 772-210-4499 or email Tim to find out more about exit planning solutions.

Ask about our complimentary proprietary tools and checklists. All inquiries are confidential.

Tim Kinane

Tim is a Consultant to Business, Government and Not-for-Profits Organizations specializing in innovative and challenging ways for organizations to survive, to thrive and to build their teams.

Tim is a Consultant to Business, Government and Not-for-Profits Organizations specializing in innovative and challenging ways for organizations to survive, to thrive and to build their teams.