Posts Tagged "Tax Cuts and Jobs Act (TCJA)"

Your Last Five Years: Where to Go From Here?

You, as a business owner, must answer five critical questions once you reach five years before your desired exit. These five questions define your exit goals and help shape the plan for how you will achieve those goals. As stated in previous articles in this series, there’s no way to sugar-coat this—answering these five questions must happen as you enter Your Last Five Years. Without clear answers, you will not know the steps needed for your exit planning, and you potentially run out of time to maximize your exit success.

This article is the final installment of a seven-part series on what business owners need to do once they reach the Last Five Years before exit.

The five critical questions are:

- What is My Likely Exit Strategy?

- How Much Do I Need to Net From My Exit?

- What Do I Want My Legacy to Be?

- What Do I Want To Do In Life After Exit?

- How Exitable is My Company?

NOTE: Click the article links above to review other installments of the ‘Your Last Five Years’ series

In the previous articles in this series, we explored the five critical questions you as a business owner must answer once you reach five years before your desired exit. As stated in these previous articles, there’s no way to sugar-coat this—answering these five questions must happen as you enter Your Last Five Years. In this last article in this series, we will discuss the remaining steps owners need to take once you reach the point where you intend to exit within the next five years.

Assemble Your Team

Once you arrive at Your Last Five years, it is time to assemble your exit advisory team. Trying to exit without professional assistance is a recipe for failure, and you have only one shot at exit success. First, there will be many highly technical issues to address during exit dealing with legal, tax, accounting, and financial matters. Second, preparing for exit takes hundreds and sometimes thousands of hours of work. You and your management team likely cannot afford to take your eyes off the company ball during the Last Five Years, so outside expert help brings needed bandwidth. Last, if you are selling your company, then your buyer realistically will have more experience doing deals than you and will exploit it against you if you don’t have your team of experts on your side.

Your advisory team can be broken down into two components, a Core Team that every business owner needs, and then a Support Team which varies by your likely exit strategy, as indicated in the chart below. (Remember, selecting your likely exit strategy is one of the questions that must be addressed when you reach Your Last Five Years.)

Once you have your Core Team identified, the next step is to meet with them as a group and share with them your answers to the five questions reviewed in this article series.

Five Exercises to Get Started

Ask any owner who has exited if, in retrospect, he or she would have started getting ready sooner and very likely he or she will advise you to get started planning your exit as early as possible. Once you reach Your Last Five Years, time will become limited and precious. Five years is only 60 months or 1,860 days. It will go by quickly.

Need additional help formulating where to go from here? Consider these final exercises to define your exit goals, and how to get started.

1. Imagine you are looking into a crystal ball, and visualize yourself five years from now, on the day immediately after you have exited. Write down exactly what you wish to see. Be as specific as possible.

2. Write down five outcomes you want to avoid in the course of your exit. Keep the list handy as you go forward.

3. List five people who can help you achieve your exit goals. Set a deadline to speak with them.

4. Describe the top five factors that could undermine your exit success. Review them with your advisory team.

5. Identify the first five people you want to thank as part of your exit plan. Share this list with your close family and advisors.

To discuss your Last Five Years, and how to plan for and achieve a successful exit, Call 772-210-4499 or email Tim to schedule a confidential, complimentary consultation.

Want to know how this all applies to you? Click here to schedule a complimentary confidential 45-minute consultation with Tim today.

Want to know how this all applies to you? Click here to schedule a complimentary confidential 45-minute consultation with Tim today.

12 Timely Questions the New Tax Laws Raise for Every Business Owner in America

The Tax Cuts and Jobs Act (TCJA) is perhaps the most sweeping US tax law change in several decades, with a long list of changes to corporate tax rates, personal income tax rates, and other areas. The new laws change much of the tax landscape for businesses and their owners—now and at exit.

Therefore, owners contemplating exit should sit down with their tax, legal, financial, and exit advisors to discuss the new laws and evaluate what steps they must take in this new world.

To aid you, listed below are 12 questions that owners should put to their advisors. We recommend owners print this list and set up a meeting with their advisory team to discuss and review:

12 Questions that Owners Should Put to Their Advisors

Under the new laws, which legal form(g., C-corporation, S-corporation, LLC, partnership, etc.) is most advantageous for our current needs? How about at exit?

Which of themany new and revised tax regulations under TCJAmay NEGATIVELY impact our business? What actions should we consider as a result?

Which of the many new and revised tax regulations under TCJA may POSITIVELY impact our business? What actions should we consider as a result?

Does TCJA contain any provisions that require us to re-evaluate our current: ownership structure, owner compensation practices, capital structure, and equipment purchasing and/or leasing plans?

Given that our likely exit strategy is to one day (Pick one):

□ Sell to an outside buyer

□ Sell to an inside buyer

□ Pass the business down to family

□ Shut the business down

Under the new tax laws, we should:

_______________________________________

(Answer with the actionable ideas discussed with your advisor)

Given that our desired exit timeframe is to exit (Pick one):

□ Within next 12 months

□ Between one and three years from now

□ Between three and five years from now

□ Between five and ten years from now

□ Longer than ten years from now

Under the new tax laws, we should: _________________________________________

(Answer with the actionable ideas discussed with your advisor)

What will my personal income tax picture look like under the new laws? (We recommend modeling them to compare before and after TCJA.)

If the new laws present a significant change (positive or negative) to my personal income tax burden, consequently, what steps should I consider to best achieve my immediate and future financial goals?

Which of the many new and revised tax regulations under TCJA may negatively impact my personal financial planning and picture? What actions should we consider as a result?

Which of the many new and revised tax regulations under TCJA may positively impact my personal financial planning and picture? What actions should we consider as a result?

What changes, if any, should I consider to my personal estate planning as a result of the new tax laws?

What else should I consider doing within my business and my personal financial affairs as a result of the new tax laws that we have not yet discussed?

We encourage you to review these questions with your trusted advisors as soon as possible.

If you would like to review your answers with a NAVIX Consultant, Call 772-210-4499 or email Tim for a complimentary 45-minute consultation.

12 questions that Owners Should Put to Their Advisors

Exit Planning Under the New Tax Laws: Should You Be a C-Corporation?

While there are many material differences between C-corporations and other legal forms, for this purpose the most important tax difference is that C-corporations pay taxes on income, whereas the other commonly used legal forms are pass-through entities, which mean taxable income (or losses) “pass-through” to the owners’ personal income tax returns. This difference is relevant because, despite the much-hyped tax cut, owners of C-corporations still face under the new tax laws the risk of double-taxation when they sell the company. If double-taxation sounds bad, that’s because it usually is.

Here’s what double-taxation means, and why it occurs. When corporations are sold, the buyer has a choice to make. Does the buyer want to purchase the corporation’s stock from whomever or whatever owns it, or does the buyer want to purchase the company’s assets from the corporation itself? The two options are thus called stock sales (a.k.a. entity sales) and asset sales. Buyers overwhelmingly prefer asset sales, for two main reasons. First, stock sales increase potential risk to buyers, because if they buy the stock, they may inherit future liabilities attached to that stock, whether known or unknown at the time of sale. The second reason buyers overwhelmingly prefer asset sales is because asset sales typically are more attractive to the buyer financially. In an asset sale, the buyer gets to depreciate on its tax return some assets faster than it commonly would be able with a stock sale. For these two reasons, buyers prefer asset sales.

Are you familiar with the adage that says in any negotiation between two parties where one has all of the money, and the other does not, the one with the money wins? Well, the adage applies here. The buyers have the money. So, more often than not, buyers get their way and require asset sales. (There is even a provision of the tax code called Section 338(h)(10) that lets buyers treat the sale as if it were an asset sale for tax purposes, even though structurally the transaction was a stock sale. This is called a deemed asset sale.)

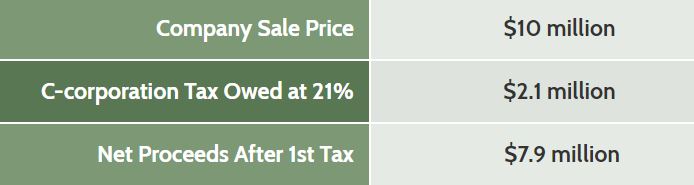

So that means if you intend to sell your company one day, the future sale most likely will be an asset sale. That’s when double-taxation kicks in. First, the buyer purchases from the corporation its assets. At that point, a C-corporation now has to pay any taxes owed from the sale of its assets. Let’s create a simple example. Assume a $10 million asset purchase price, and the company pays exactly 21% in taxes, which is $2.1 million.

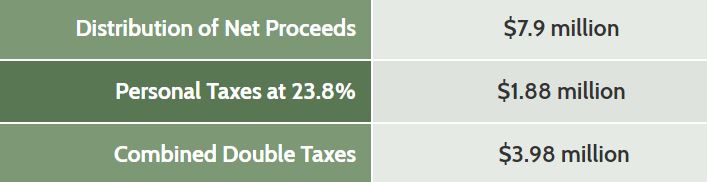

Once the dust has settled, the seller is now left with an empty C-corporation, other than the $7.9 million in after-tax cash from the sale proceeds sitting in the company’s bank account. At that point, the seller wants to take money home thank-you-very-much, and so distributes the money out to the owner(s). That triggers the second tax. Let’s assume that second tax is all long-term capital gains taxes at 20%, plus the 3.8% Net Investment Income Tax that usually applies. So now that’s another $1.88 million in personal taxes ($7.9 million X .238) as shown below. Put the two levels of tax together, and the total taxes paid at sale are about $3.98 million on the original $10 million sale.

The double-taxation creates almost a 40% total tax burden—and this example does not include any state or local taxes, which would only add to the total. So, even though the C-corporation tax rate is reduced, if you intend to sell your company one day to an outside buyer, it remains highly disadvantageous to sell your business while a C-corporation in most situations.

One last important point to remember: If you have a company that is a C-corporation that you expect to sell, and to avoid double-taxation you usually would convert that C-corporation into an S-corporation. However, you must outwait that conversion by five years to eliminate all risk of double-taxation at sale. This arcane tax provision is called the Built In Gains tax—yes, the BIG tax. We can’t make this stuff up.

Operating as a C-corporation may only be advantageous if you are confident that you will not sell the company for any reason within the next five years, or if you never intend to sell your business but instead you give it to family members in the future. All of this reinforces that business owners need to think through their exit and plan ahead on tax questions, many years prior to exit.

This information is for educational purposes only. Please consult your tax, legal, and other advisors to evaluate how this material may apply to you and your businesses. NAVIX does not provide tax or legal advice nor services.

Call 772-210-4499 or email Tim to find out more about exit planning solutions.

Call 772-210-4499 or email Tim to find out more about exit planning solutions.

Ask about our complimentary proprietary tools and checklists. All inquiries are confidential.

Tim Kinane

Tim is a Consultant to Business, Government and Not-for-Profits Organizations specializing in innovative and challenging ways for organizations to survive, to thrive and to build their teams.

Tim is a Consultant to Business, Government and Not-for-Profits Organizations specializing in innovative and challenging ways for organizations to survive, to thrive and to build their teams.